Home Equity Loans vs. Equity Loans: Understanding the Differences

Home Equity Loans vs. Equity Loans: Understanding the Differences

Blog Article

Secret Aspects to Consider When Using for an Equity Loan

When considering getting an equity loan, it is important to navigate through numerous crucial elements that can significantly impact your financial health - Home Equity Loans. Understanding the kinds of equity finances available, reviewing your qualification based on financial aspects, and meticulously analyzing the loan-to-value ratio are crucial preliminary steps. Nevertheless, the intricacy strengthens as you look into comparing rate of interest prices, charges, and settlement terms. Each of these variables plays an essential function in determining the overall cost and expediency of an equity loan. By thoroughly inspecting these components, you can make informed decisions that straighten with your long-term monetary goals.

Kinds of Equity Loans

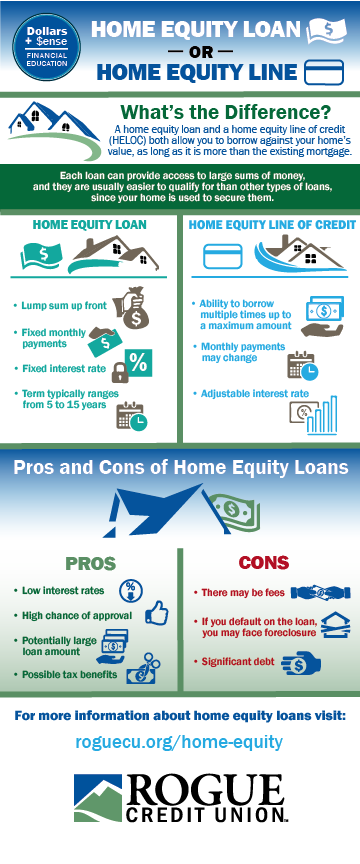

Different monetary institutions use a variety of equity car loans customized to fulfill diverse loaning requirements. One usual kind is the standard home equity financing, where homeowners can obtain a lump amount at a fixed interest price, using their home as security. This kind of lending is suitable for those who require a large amount of cash upfront for a details function, such as home renovations or financial obligation loan consolidation.

Another popular alternative is the home equity line of credit score (HELOC), which operates more like a charge card with a revolving credit rating restriction based on the equity in the home. Customers can attract funds as needed, up to a specific limitation, and just pay rate of interest on the quantity made use of. Home Equity Loans. HELOCs are suitable for ongoing costs or projects with unclear prices

Furthermore, there are cash-out refinances, where property owners can refinance their current mortgage for a higher amount than what they owe and receive the difference in money - Alpine Credits. This sort of equity funding is helpful for those wanting to benefit from reduced rates of interest or access a large amount of cash without an additional regular monthly settlement

Equity Car Loan Qualification Variables

When taking into consideration eligibility for an equity funding, monetary institutions generally analyze elements such as the candidate's credit history, earnings stability, and existing financial obligation obligations. A crucial aspect is the credit history, as it shows the borrower's credit reliability and ability to settle the lending. Lenders favor a greater credit history, usually over 620, to minimize the threat connected with borrowing. Revenue security is an additional key variable, showing the debtor's ability to make normal finance payments. Lenders might need proof of constant revenue with pay stubs or tax returns. Additionally, existing debt commitments play a substantial role in figuring out qualification. Lenders evaluate the borrower's debt-to-income proportion, with lower ratios being much more desirable. This ratio indicates just how much of the consumer's income goes in the direction of settling financial obligations, influencing the lending institution's decision on loan authorization. By thoroughly analyzing these variables, financial institutions can establish the candidate's eligibility for an equity finance and establish appropriate financing terms.

Loan-to-Value Ratio Factors To Consider

A reduced LTV ratio suggests much less risk for the lending institution, as the debtor has even more equity in the home. Lenders generally prefer reduced LTV proportions, as they offer a better padding in instance the borrower defaults on the car loan. A greater LTV proportion, on the other hand, recommends a riskier financial investment for the lending institution, as the customer has much less equity in the residential property. This might result in the loan provider enforcing higher rates of interest or stricter terms on the funding to mitigate the increased risk. Customers must aim to maintain their LTV proportion as reduced as feasible to improve their possibilities of authorization and protect much more beneficial lending terms.

Interest Prices and Fees Comparison

Upon assessing rates of interest and fees, borrowers can make informed choices concerning equity car loans. When contrasting equity funding alternatives, it is important to pay very close attention to the rate of interest prices provided by different loan providers. Rate of interest can substantially impact the overall cost of the financing, impacting regular monthly settlements and the overall amount settled over the finance term. Lower rates of interest can cause substantial cost savings gradually, making it crucial for borrowers to look around for the most competitive prices.

Aside from passion prices, consumers should likewise think about the various charges connected with equity finances. Prepayment fines may use if the consumer pays off the financing early.

Payment Terms Assessment

Efficient analysis of payment terms is crucial for debtors looking for an equity financing as it directly impacts the loan's affordability and economic results. When assessing settlement terms, debtors ought to very carefully assess the funding's duration, monthly payments, and any kind of prospective charges for very early repayment. The lending term refers to the size of time over which the borrower is anticipated to repay the equity car loan. Much shorter lending terms typically cause greater month-to-month repayments yet lower total passion costs, while longer terms supply lower regular monthly repayments however may result in paying more rate of interest over time. Consumers require to consider their economic scenario and goals to identify the most suitable repayment term for their demands. Furthermore, recognizing any type of fines for very early payment is necessary, as it can affect the flexibility and cost-effectiveness of the financing. By completely reviewing settlement terms, customers can make enlightened choices that straighten with their monetary goals and make sure successful lending monitoring.

Final Thought

In verdict, when looking for an equity car loan, it is very important to think about the kind of financing available, eligibility aspects, loan-to-value ratio, rates of interest and fees, and payment terms - Alpine Credits Canada. By thoroughly reviewing these crucial elements, debtors can make enlightened choices that straighten with their monetary objectives and circumstances. It is crucial to completely research study and contrast alternatives to guarantee the very best feasible end result when seeking an equity funding.

By thoroughly evaluating these factors, economic resource organizations can figure out the applicant's eligibility for an equity finance and establish suitable car loan terms. - Equity Loans

Interest rates can significantly influence the general price of the finance, influencing regular monthly payments and the complete amount settled over the finance term.Effective assessment of payment terms is critical for consumers looking for an equity lending as it directly affects the lending's cost and financial results. The funding term refers to the length of time over which the consumer is anticipated to repay the equity finance.In verdict, when using for an equity loan, it is vital to think about the type of car loan readily available, eligibility factors, loan-to-value ratio, interest prices and fees, and payment terms.

Report this page